All those who live abroad may also be required to pay taxes in Spain: in addition to foreigners who may be owners of a property, we also have almost three million Spaniards who reside abroad.

All those who live abroad may also be required to pay taxes in Spain: in addition to foreigners who may be owners of a property, we also have almost three million Spaniards who reside abroad.

As a general rule individuals pay taxes in the country they have their residence, except for American citizens who are also required to declare their income in the United States, due to their citizenship, but in any case, the Spanish Tax Law obliges non-residents to pay taxes in Spain regardless of their nationality, who have economic interests in Spain, whether in the form of income or assets.

On one hand, there is the income from work in Spain of a non-resident that is paid at a tax rate of 24%. This is the case of foreign teachers who arrive to work in the month of September and that calendar year are considered non-residents.

On the other hand, we have all those individuals who have a property in Spanish territory, either for personal use or to rent, they also have to pay taxes:

If the home is for personal use, they must declare an annual imputed real estate income of 2% (1.1% if the cadastral value has been reviewed in the last ten years) of the Cadastral Value at a rate of 24% (19% for residents of the EU), an annual payment is made.

If the property is rented, non-residents must declare the income obtained on a quarterly basis, at a tax rate of 24%, and no expenses can be deducted.

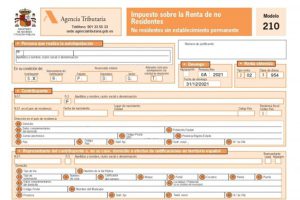

In all cases, the tax is self-assessed through Model 210, a form that brings together all the declarations, which makes the different codes for the different options a bit complicated.

The form can only be submitted online through the Tax Agency website.

If you have any questions or are unable to file it, please do not hesitate to contact US Tax Consultants. Tel. +34 915 194 392 info@ustaxconsultants.es

0 Comments